Ameris Bancorp: Mortgage Banking Normalization To Counter Loan Growth (NASDAQ:ABCB)

")

Earnings of Ameris Bancorp (NASDAQ: ABCB) shot up this year mostly due to a remarkable surge in mortgage banking revenues. The normalization of mortgage refinancing activity over the next two years will likely reduce mortgage banking revenues next year relative to 2020. Although ABCB is unlikely to repeat the good performance of 2020 in 2021, earnings next year will most probably remain elevated above the pre-pandemic level. The reopening of the economy will lead to a decline in provision expense, which in turn will support the bottom-line. Additionally, ABCB’s loans are likely to continue to grow on the back of management’s expansion efforts. Overall, I’m expecting ABCB to report earnings of $3.92 per share in 2021, down 4% from my expected earnings for 2020, but up 42% from actual 2019 earnings. Next year’s target price suggests a high upside from the current market price; therefore, I’m bullish on ABCB.

Mortgage Banking Normalization to Drag Earnings

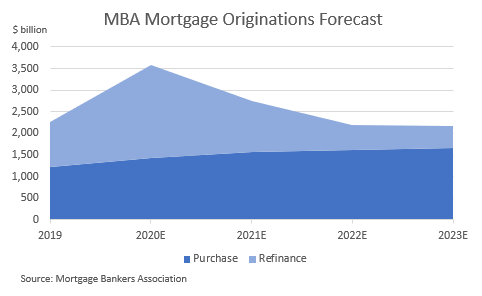

ABCB’s mortgage banking revenue surged to $279 million in the first nine months of 2020 from $86 million in the corresponding period last year. The 225 basis points decline in Federal Funds rate over the past year and a half was the major catalyst for mortgage banking activity. The Federal Funds rate will likely remain stable through 2023, as projected by the Federal Reserve. Consequently, the incentive to refinance will taper off, leading to a decline in refinancing activity over the next couple of years. The Mortgage Bankers Association (“MBA”) expects the refinance origination volume to decline almost linearly over the next two years towards a normal level. The following chart shows the MBA’s latest forecasts.

I’m expecting the mortgage banking revenue to decline to a run rate of $60 million by the fourth quarter of 2021. Based on the mortgage banking forecast, I’m expecting ABCB to report a non-interest income of $377 million in 2021, down 22% from 2020.

Expansion Efforts to Drive the Loan Portfolio

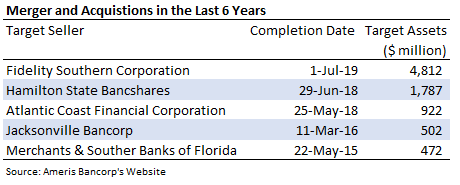

ABCB’s loans have grown strongly over the past through merger and acquisition activity as well as organic growth. The following table from ABCB’s website gives an overview of the company’s recent acquisition history.

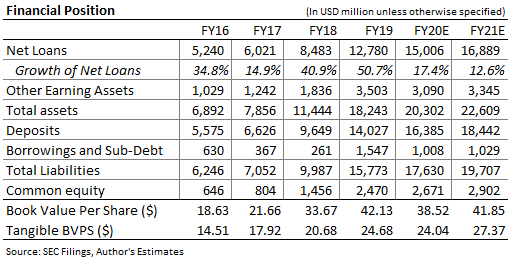

I’m expecting ABCB’s loans to continue to grow in 2021 despite headwinds from a slow economic recovery and uncertainties related to the efficacy of the COVID-19 vaccination program. The management mentioned in the third quarter’s conference call that they have hired new talent in commercial treasury and intend to continue to hire bankers, especially in Augusta, GA. The management also mentioned in the conference call that the banking industry may witness significant M&A activity as the pandemic ends; however, I have ignored this factor in my forecasts in order to be prudent. On the other hand, the upcoming forgiveness of $1.1 billion worth of existing Paycheck Protection Program (“PPP”) loans will constrain the loan growth. Considering these factors, I’m expecting loans to grow by 12.6% by the end of 2021 from the end of December 2020. The following table shows my estimates for loans and other balance sheet items.

A reduction in yields will likely partly offset the impact of loan growth on net interest income. The average portfolio yield will likely continue to decline as higher-yielding loans mature and new lower-yielding loans get originated. However, the company has significantly improved its deposit mix over the last two quarters, which will ease the pressure on net interest margin (“NIM”) going forward. The proportion of non-interest bearing deposits in total deposits increased to 36.8% by the end of September, from 30.5% at the end of March 2020. Considering these factors, I’m expecting the NIM to decline by around three basis points sequentially in each quarter of 2021. Based on the loan and NIM projection, I’m expecting ABCB’s net interest income to increase by 5.4% year-over-year in 2021.

Provisions Expense Likely to Trend Downwards as the Economy Recovers

ABCB’s provision expense declined to $18 million in the third quarter from $88 million in the second quarter of 2020. The provision expense will likely continue to decline as the economy recovers from the pandemic next year. Additionally, ABCB’s credit risk has substantially declined of late, which will keep the need for provisioning low. As mentioned in the third quarter’s investor presentation, loans on deferral made up less than 5% of total loans as of October 15, 2020, down from a peak of 20% of total loans, excluding PPP. Considering these factors, I’m expecting ABCB to report a provision expense of $60 million in 2021, down from my estimated provision expense of $162 million in 2020.

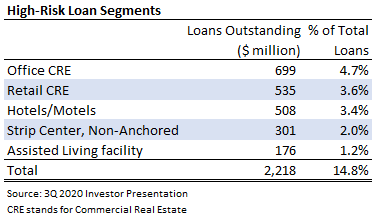

However, ABCB’s credit risk is not yet back to normal because of the company’s exposure to pandemic-sensitive loan segments. If the pandemic worsens beyond expectations, then these loan segments can have a detrimental impact on earnings. The following table shows ABCB’s exposure to loan segments that are vulnerable in my opinion.

Expecting Earnings of $3.92 per Share in 2021

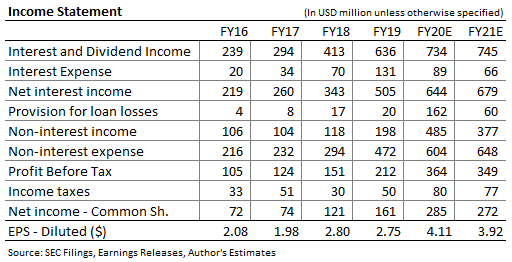

The normalization of refinancing activity will likely decrease earnings next year on a year-over-year basis. On the other hand, lower provision expense and loan growth will likely support earnings. The team expansion discussed above will likely lift expenses in the coming quarters; however, the management hopes to counter the increase in salary expense through branch closures, as mentioned in conference call. According to details given in the third quarter’s investor presentation, ABCB closed eight branches in October 2020. Further, the company planned to convert two branches to drive-thru only and it planned to close another branch. Overall, I’m expecting ABCB to report earnings of $3.92 per share in 2021, down 4% from my estimated earnings for 2020. Despite the year-over-year decline, the earnings for next year will likely remain much higher than the pre-pandemic level mostly due to the loan growth. The expected earnings for 2021 are 42% higher than ABCB’s earnings for 2019. The following table shows my income statement estimates.

Actual earnings may differ materially from estimates because of the risks and uncertainties related to the timing and efficacy of mass COVID-19 immunization.

Valuation Analysis Suggests a High Upside

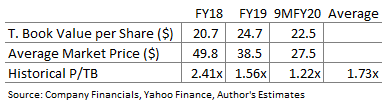

I’m using the historical price-to-tangible book multiple (“P/TB”) to value ABCB. The stock has traded at an average P/TB ratio of 1.73 in the past, as shown below.

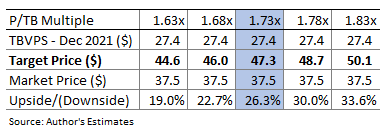

Multiplying the average P/TB multiple with the forecast tangible book value per share of $27.4 gives a target price of $47.3 for the end of next year. This price target implies a 26% upside from the December 24 closing price. The following table shows the sensitivity of the target price to the P/TB ratio.

Apart from the upside, ABCB is also offering a low dividend yield of 1.6%, assuming the company maintains its quarterly dividend at the current level of $0.15 per share. There is little threat of a dividend cut because the earnings and dividend estimates suggest a payout ratio of just 15% for 2021.

Based on the high potential price upside, I‘m adopting a bullish rating on ABCB. Despite the outlook of mortgage banking revenue decline, I like the company because of its strong loan growth prospects.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Disclaimer: This article is not financial advice. Investors are expected to consider their investment objectives and constraints before investing in the stock(s) mentioned in the article.