Genesis Energy: A Few Opportunities But Debt Load Is Concerning (NYSE:GEL)

")

Genesis Energy, L.P. (GEL) is a rather unique midstream partnership because it operates in some segments that we do not see in other businesses. The company suffered from some financial trouble a few years ago but was beginning to recover when the pandemic hit, forcing it to join the ranks of midstream companies that cut their distribution following the outbreak. As has been the case with many such companies, this had a devastating effect on the unit price and Genesis Energy is down 67.82% year-to-date. However, there are a few things that could ultimately help the company recover once the economy does but the near-term environment will continue to pose challenges for it. Thus, it would still be a good idea to remain cautious.

About Genesis Energy

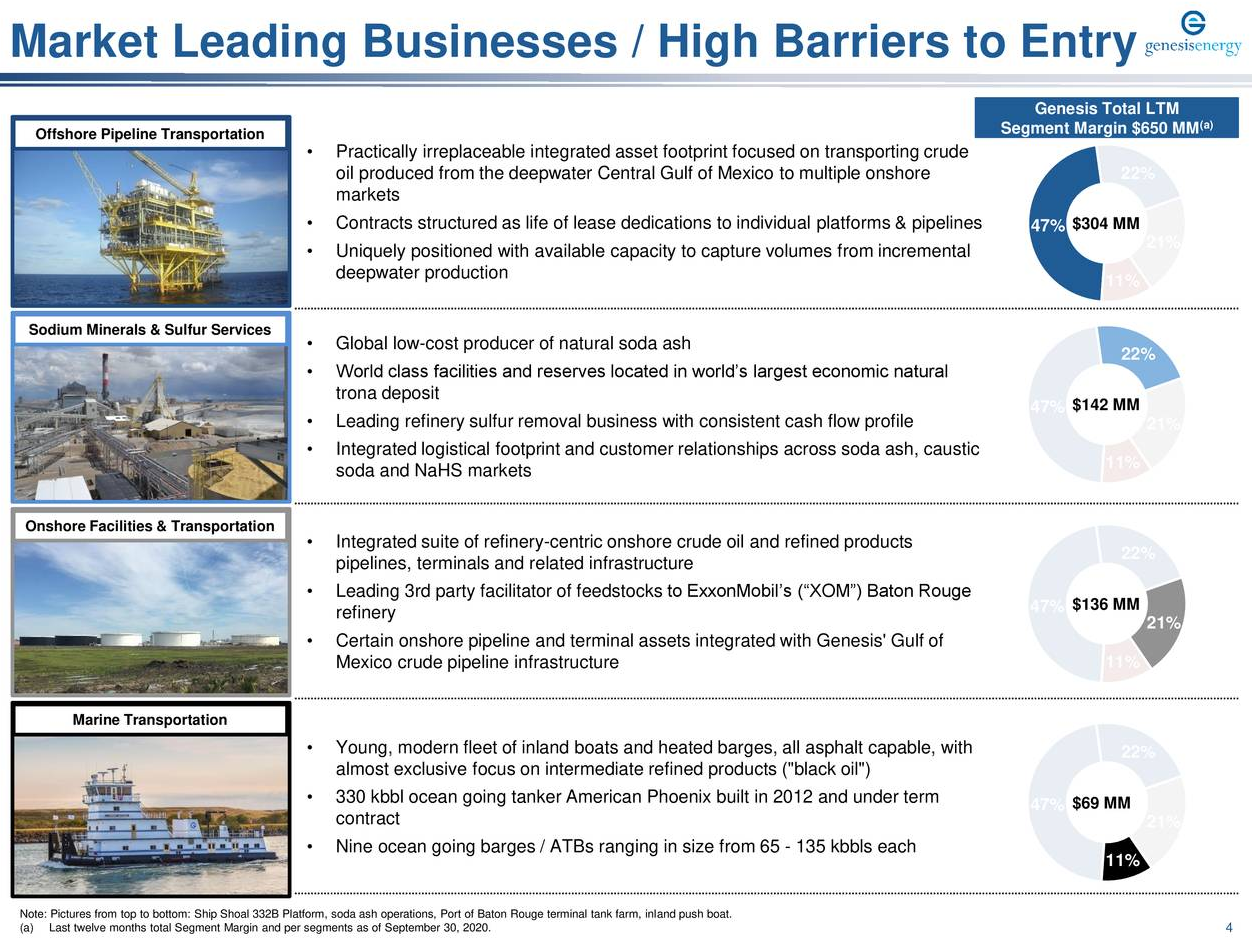

As mentioned in the introduction, Genesis Energy is a somewhat unique midstream company due to the fact that it operates in a diverse array of segments that are not often found at other midstream companies. These segments are offshore pipelines, onshore pipelines, marine transportation, and sodium minerals and sulfur services:

Source: Genesis Energy

Source: Genesis Energy

When we think of a midstream company, we most often think of a pipeline operator like Kinder Morgan (KMI). This most resembles Genesis Energy’s onshore pipelines unit, which accounts for about 21% of the company’s segment margin (akin to gross profit). The company’s onshore transportation unit operates a few pipelines around the Gulf Coast but mostly focuses on terminals:

Source: Genesis Energy

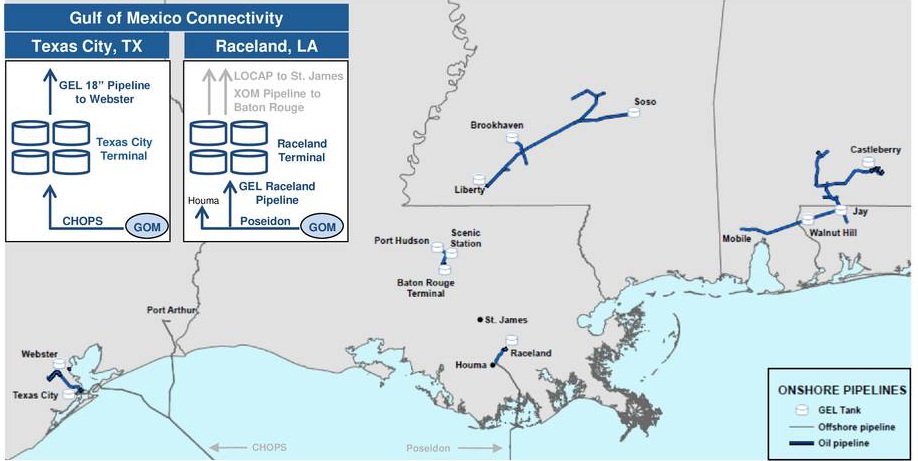

An oil terminal is simply a large industrial facility where oil and oil-related products are stored until they are sent out to some other location like a refinery, oil tanker, or pipelines. It’s also where all different types of midstream transportation come together for loading and unloading purposes. Genesis Energy owns three of these terminals, including the massive Baton Rouge Complex that’s an integral part of Exxon Mobil’s (XOM) refinery complex in the area and also has connections to both railways and docks that support oceangoing ships. As might be expected, a good portion of the revenues from this facility come from a number of take-or-pay contracts with Exxon Mobil. We can therefore assume that this revenue is going to be relatively secure since it seems rather unlikely that Exxon Mobil will default on any contracts with a facility that’s critical to one of its largest refineries in the United States.

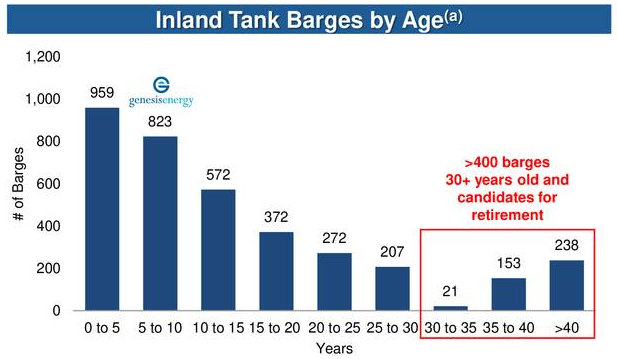

Genesis Energy also operates a marine transportation network, which is not something that we see very often among midstream companies. This also is an element of Genesis Energy’s business that has been struggling for a few years. As might be guessed, this business unit primarily transports hydrocarbon products via barges traveling on inland waterways such as rivers. Unfortunately, the business unit has been struggling for a while because of an industry-wide oversupply of these barges that has kept dayrates suppressed. This business operates very much like the oceangoing industry in that a company that needs something shipped will hire the services of a barge at a market-based dayrate. This can be done under extended contracts as opposed to a single trip but multi-year contracts are fairly rare.

Fortunately, there may be some early signs that things may start to improve in this sector of the company’s business. This actually might have been a side effect of the pandemic as companies all across the energy sector have begun to look for areas in which they can reduce costs. One way in which this can be accomplished is to retire old barges that have become uneconomic to operate. Nationwide, there are more than 400 barges that fall into this category and so might begin to be retired:

Source: Genesis Energy

If this does indeed play out then it will naturally reduce the oversupply of barges in the market and thus should ultimately prove to be a positive for dayrates. An increase in dayrates will naturally prove to be a positive for Genesis Energy since it will increase the revenues and cash flows from this business unit. Admittedly though, it does remain to be seen if this scenario will ultimately play out.

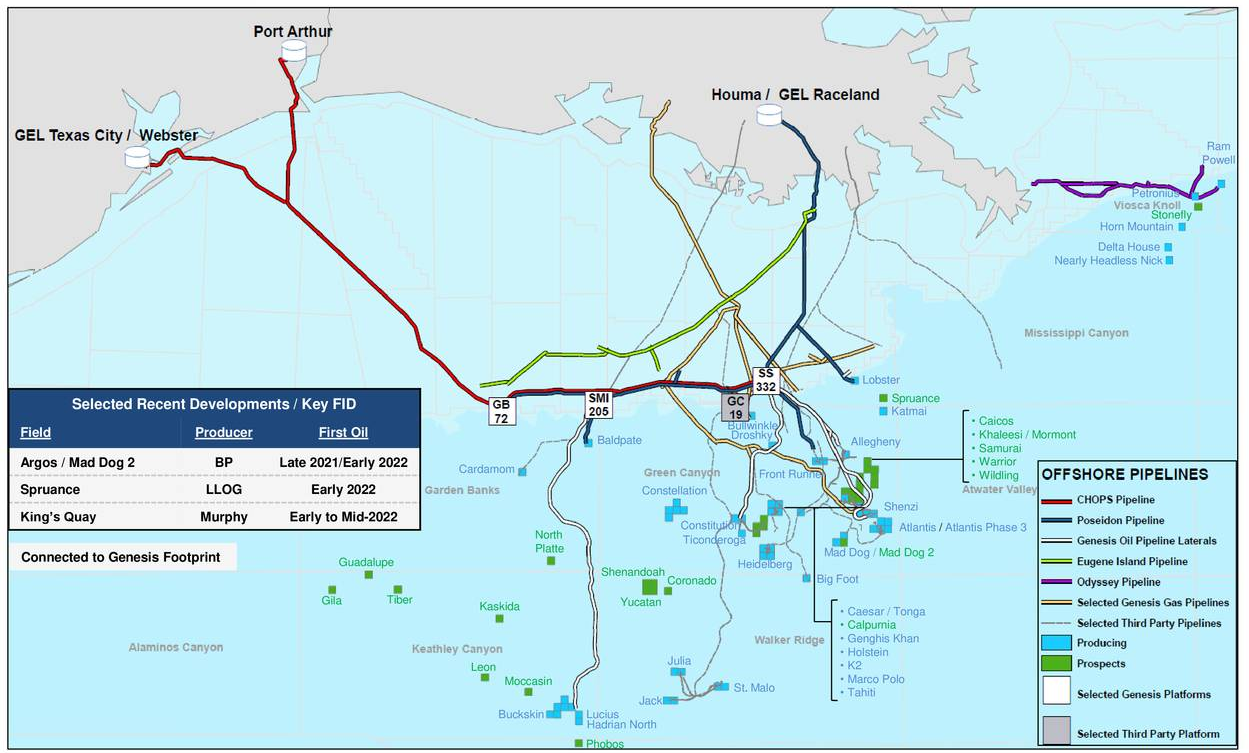

Genesis Energy also is one of the largest operators of offshore pipelines in the Gulf of Mexico. An offshore pipeline is essentially the same thing as an onshore pipeline except that it travels through the water. Basically, it transports gas and oil from an offshore well to the shore.

Source: Genesis Energy

Source: Genesis Energy

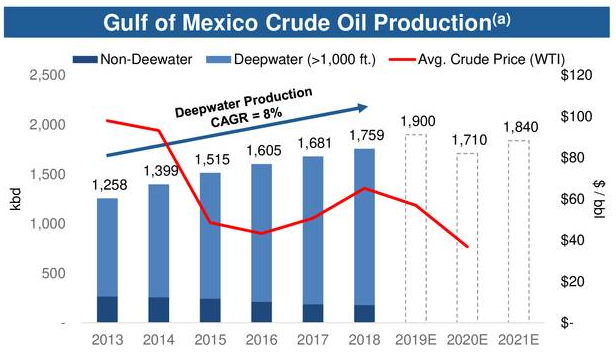

The Gulf of Mexico is not an area that we hear a great deal about in the media as it has largely been overshadowed by the production growth in areas like the various shale plays, but it has certainly seen its share of production growth, most of which was in deepwater or ultra-deepwater areas. In fact, over the 2013 to 2019 period, deepwater crude oil production in the Gulf of Mexico grew at an 8% compound annual growth rate. It was down this year due to the pandemic but is expected to recover somewhat next year:

Source: Genesis Energy

The story also looks promising beyond 2021 and Genesis Energy is well positioned to take advantage of it due to the position of the company’s infrastructure. This is due to the fact that a few of the company’s pipelines are located near projects coming online in early 2022 and so can easily be connected to service them. These projects include BP’s (BP) Mad Dog 2, LLOG’s Spuance, and Murphy Oil’s (MUR) King’s Quay. I have discussed a few of these projects in previous articles on the respective companies. The reason why these projects coming online will benefit Genesis Energy is volumes. As with any other midstream company, Genesis Energy derives revenue by charging a fee for each unit of oil or natural gas that moves through its pipelines. As these new projects come online, it should increase the volume of resources moving through the company’s pipes and thus result in both revenue and cash flow growth for the company in 2022. This is especially true because Genesis Energy’s pipelines are nowhere near capacity so have plenty of room to accommodate new production.

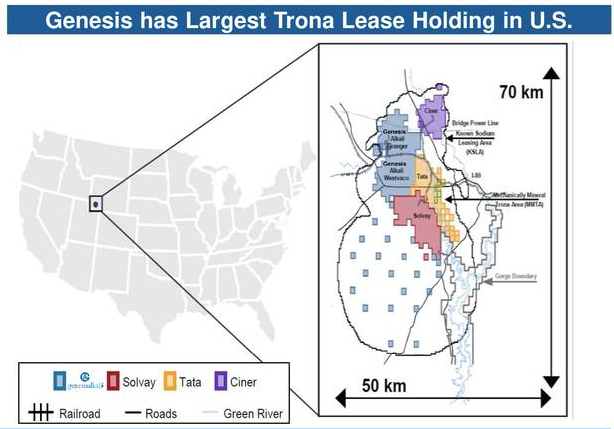

Genesis Energy also is the largest producer of natural soda ash in North America. This is something that differentiates the partnership from pretty much every other midstream company as few of them have any operations outside of traditional midstream functions. This business is something that investors should appreciate though as the soda ash production business provides a nice anchor of stability for Genesis Energy. The company’s natural soda ash production comes from the company’s position as the largest leaseholder in the largest trona deposit in the world, which contains over 80% of the world’s economically-viable soda ash:

Source: Genesis Energy

Genesis Energy produces about 3.5 million tons of natural soda ash at the site. Natural soda ash is a critical component in many of the products that we all use in our everyday lives including glass, soap, detergents, and other chemicals. These are all products that always are in demand, even during recessions and the recent pandemic, so it’s unlikely that the demand for natural soda ash will be going away anytime soon. Thus, we can see how this would prove to be a stable business for Genesis Energy.

We can see further evidence of this demand stability by looking at the prevailing market price for natural soda ash. As is the case with the price of other commodities, the price of natural soda ash is generally set by supply and demand. Thus, if the price is relatively stable, we can assume that the same is true of demand. As we can clearly see, that is indeed the case:

Source: United States Geological Survey, Genesis Energy

As we can see, with the notable exception of the years around the financial collapse, the overall price of natural soda ash has been almost perfectly flat. In fact, even during the worst years of that recession, the price was not very far off of its average level. Thus, we can indeed conclude that this is a very stable business that provides a certain measure of support to the distribution.

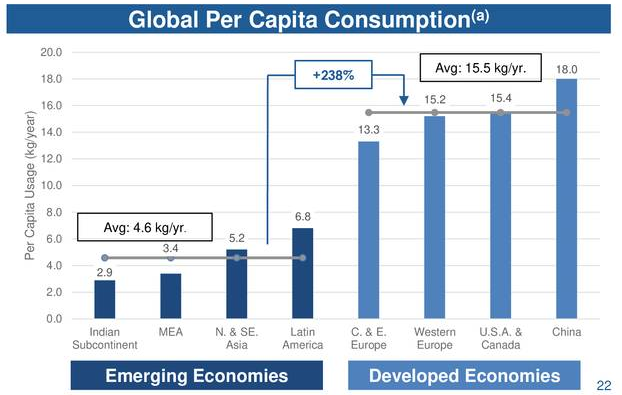

There’s also the potential for some growth in natural soda ash demand from the various emerging economies around the world. This growth comes from the emerging middle class in those nations, which still has a lifestyle that is somewhat meager compared to its counterparts in the developed nations. This is beginning to change however and as these individuals have become wealthier, they have begun to demand some of the same luxuries that developed nation citizens enjoy, which include those products that are manufactured using natural soda ash. This could have a major impact on demand, as shown here:

Source: IHS Markit, Genesis Energy

As we can clearly see, the developing nations consume substantially less natural soda ash per capital than the developed nations do. Thus, the global demand for the substance could very easily increase dramatically as this gap is closed. This could prove to be a net positive for Genesis Energy as its enormous reserves make it one of the few companies that could increase its production in order to meet this demand.

The company already has begun work on doing just this through the expansion of its Granger facility. This is a $330 million project that’s intended to increase the facility’s production by approximately 750,000 tons per year. As Genesis Energy currently only produces about 3.5 million tons of natural soda ash annually, we can clearly see that the project will substantially increase Genesis Energy’s production of the compound. The company has two motivations behind doing this project now. The first is obviously to position the company to profit off of the forthcoming demand growth in emerging markets for natural soda ash. However, this is a very long-term story that does not really justify doing this large of a project today. The company’s primary motivation here appears to be capturing some of the market that’s meeting its soda ash demand with synthetic sources. Currently, about 70% of the world’s soda ash demand is met with synthetic soda ash. However, Genesis Energy’s marginal cost of production is less than 50% that of synthetic production so the company should be able to significantly beat its competitors on price and thus take some of their business. This would obviously be good for Genesis Energy’s cash flows.

Financial Considerations

As we have seen in various previous articles on Genesis Energy, one of the company’s biggest problems has been its relatively high level of debt. While it was making some progress addressing that heading into this year, the pandemic set it back. Thus, it would be a good idea to analyze this as we think about the company.

Let us begin by looking at the way that the company finances itself. This is important because debt is a riskier way to finance a company than equity is. This is due to the fact that the company has to make regular payments on its debt if it wishes to remain solvent but there’s no such requirement with equity. Thus, should some event happen that causes the company’s cash flow to decline then such an event could push the firm into bankruptcy if it’s too highly levered. In addition to this, debt must be completely paid back at maturity. This can be accomplished by either using cash or by issuing new debt to pay off the old debt (this method is more common). However, if the market is not amenable to the company’s debt for whatever reason and the company does not have a mountain of cash then either of these scenarios could be problematic. A company financing itself with equity does not have any of these problems.

As of Sept. 30, 2020, Genesis Energy had $3.322224 billion in net debt compared to only $941.895 million in partners’ capital. This gives the company a net debt-to-equity ratio of 3.53. This is far above the ratio that I normally like to see. As a general rule, I do not like to see this figure much above 1.0 for a midstream company. While midstream companies are generally more stable entities than their upstream cousins, when the market turns unfavorable to the industry, as it did once the pandemic hit, it becomes highly difficult for any company to raise financing no matter what part of the industry it is in. A highly levered company will likely have even more trouble. Thus, Genesis Energy’s high debt load could represent a very real risk.

Naturally, the company’s ability to carry its debt is more important than just the raw amount of debt. In order to judge this, we look at the leverage ratio, also known as the debt-to-adjusted EBITDA ratio. This ratio essentially tells us how long it will take the company (in years) to completely pay off its debt if it devotes all of its pre-tax cash flow to that task. As of Sept. 30, 2020, that ratio stood at 5.25x based on the company’s annualized third quarter 2020 adjusted EBITDA. As a general rule, analysts consider anything over 5.00x to be risky. I however prefer to be more conservative and like to see this ratio under 4.00x to feel comfortable with the company’s leverage. Genesis Energy’s current ratio is well above both of these levels, so the debt could very easily pose a problem if the firm cannot maintain its cash flow. With that said, management does have the long-term goal of getting this ratio down to 4.00x, which is admirable, but I will admit that I’m nervous about the risks here.

Distribution Analysis

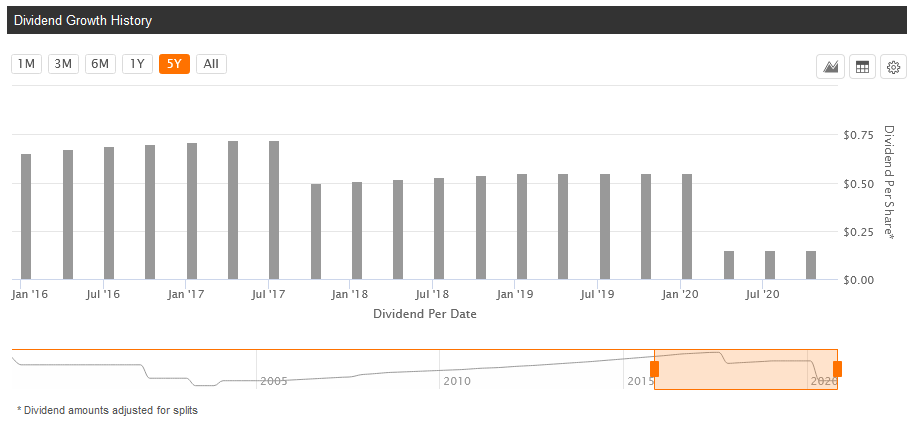

Genesis Energy has something of a troubled distribution history. The company first cut its distribution back in the second half of 2017 in order to redirect its cash flow to debt repayment. It was beginning to make some progress at doing this and then the pandemic broke out, forcing the company to cut its distribution a second time:

Source: Seeking Alpha

The company currently boasts a 9.10% yield with this new reduced distribution, due mostly to the fact that the company’s unit price is down a fairly substantial 67.82% year-to-date. We do still of course want to analyze the company’s ability to afford this distribution as we certainly do not want to risk another distribution cut. Unlike many other midstream companies, Genesis Energy does not report distributable cash flow but it does report something that it calls “available cash before reserves,” which is essentially the same thing. In short, this is a non-GAAP measure that theoretically tells us the amount of cash that was generated by the company’s ordinary operations that can be distributed to the limited partners. In the third quarter of 2020, this figure was $70.7 million but the current distribution only costs the company $18.7 million. This gives the company a very impressive distribution coverage ratio of 3.84x and a great deal of extra money that it can use for other purposes. This excess cash could be very useful for helping the company get that debt load under control. We can also see that it should be able to afford the distribution even if the cash flow declines by quite a lot.

Conclusion

In conclusion, Genesis Energy is a diversified and fairly unique midstream company and this may provide it with some opportunities going forward. In particular, the company’s offshore pipelines could see performance improvements in the near future as could its natural soda ash business. Unfortunately though, the company’s very high debt load poses some concerns. Genesis Energy already has been forced to cut its distribution twice in three years and while it does look like it can maintain its current distribution level, the company’s debt load still worries me. Management needs to address this issue.

At Energy Profits in Dividends, we seek to generate a 7%+ income yield by investing in a portfolio of energy stocks while minimizing our risk of principal loss. By subscribing, you will get access to our best ideas earlier than they are released to the general public (and many of them are not released at all) as well as far more in-depth research than we make available to everybody. We are currently offering a two-week free trial for the service, so check us out!

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: This article was originally posted to Energy Profits in Dividends prior to the market open on December 24, 2020. Subscribers have had since that time to act on it.