Monetary Security Oversight Council Is Lacking An Possibility To Increase Preparedness And Reaction To Monetary Security Threats

/https://specials-images.forbesimg.com/imageserve/5fda3a238ce1ea79dc361789/0x0.jpg "Monetary Security Oversight Council Is Lacking An Possibility To Increase Preparedness And Reaction To Monetary Security Threats")

The GAO deserves praise for its complete examination of leveraged lending and collateralized mortgage … [+]

In examining the leveraged lending and Collateralized Mortgage Obligation (CLO) marketplaces, the U.S. Authorities Accountability Workplace uncovered there are additional options for the Fiscal Balance Oversight Council (FSOC) to prepare and react to economical security threats. FSOC has been monitoring risks that come up in the leveraged lending marketplace, by way of its every month Systemic Chance Committee meetings. In its report produced right now, the GAO stated that “FSOC does not conduct tabletop or identical scenario-based mostly exercise routines wherever participants examine roles and responses to hypothetical emergency scenarios. As a consequence, FSOC is missing an possibility to boost preparedness and take a look at members’ coordinated response to economic stability challenges.” Thus much, FSOC has not publicly agreed with the GAO’s suggestion to perform tabletop workouts.

Moreover, the GAO reiterated as it experienced in 2016, that “FSOC does not typically have apparent authority to deal with broader dangers that are not certain to a specific monetary entity, these types of as threats from leveraged lending. The GAO advised that “Congress need to consider improved aligning FSOC’s authorities with its mission to react to systemic hazards.” Sadly, as of currently, Congress has not followed GAO’s advice.

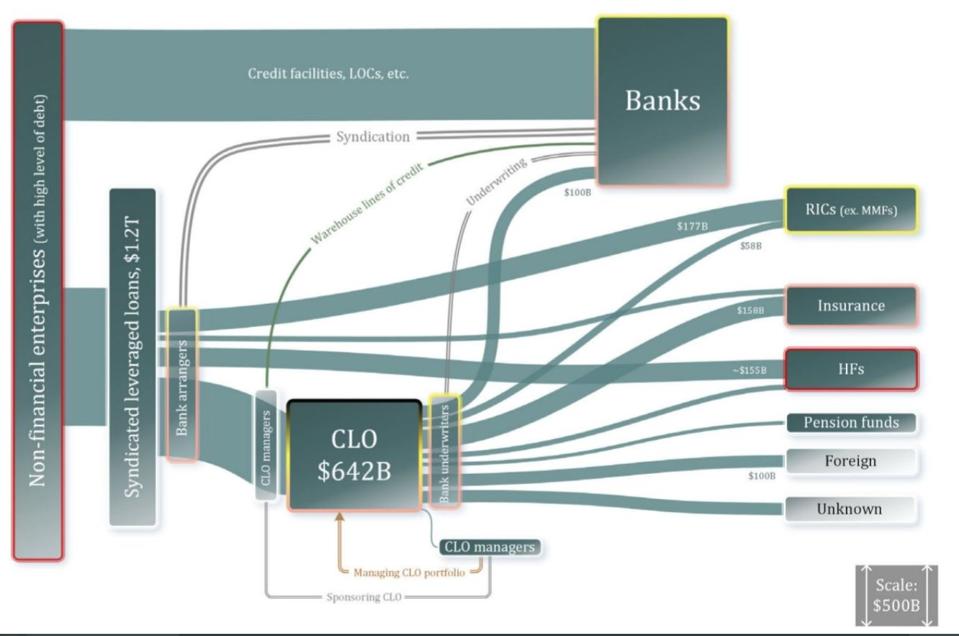

FSOC is tasked with responding to systemic risks, but in accordance to the GAO, “it may absence the instruments essential to do so comprehensively, specifically when the risks stem from wide-based functions like leveraged lending that involve a vary of financial institution and nonbank members overseen by multiple financial regulators.” GAO argues that modifications such as broader designation authority would support FSOC answer to pitfalls from routines that entail many regulators, this kind of as leveraged lending. This is specifically critical, because the 3 nationwide lender regulators, the Federal Reserve, the Workplace of the Comptroller of the Currency, and the Federal Deposit Coverage Firm, alongside with the Securities and Trade Commission all share tasks about supervising economical and non-monetary corporations involved in the leveraged lending industry additionally state financial regulators also supervise banking companies and non-banks in their states, which are in these marketplaces as leveraged mortgage originators, sellers, and buyers in collateralized personal loan obligations.

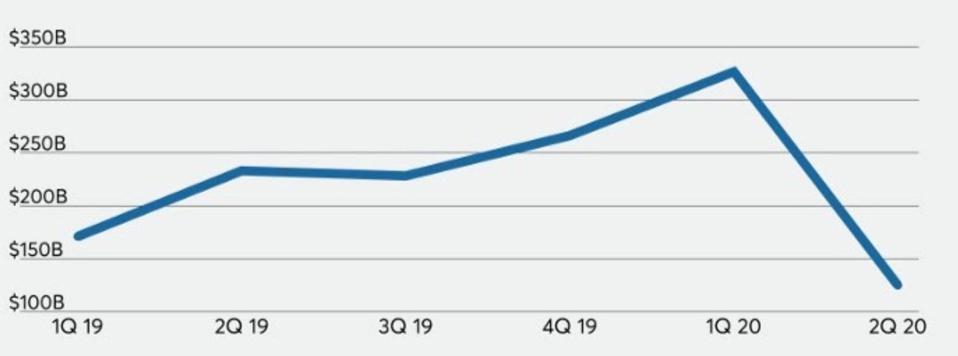

Leveraged lending had risen significantly starting up in 2013, but lessened dramatically when COVID-19 … [+]

The GAO analysis also identified that regulators do not determine leveraged lending as a major menace to economic steadiness. Nonetheless threats keep on being, in particular as the COVID-19 disaster proceeds to pressure leveraged companies’ skill to remain present on their loan payments. Before the COVID-19 disaster and this 12 months, I revealed above 35 article content citing my issues about the possible adverse affect to banking companies, other loan providers, and traders from weak underwriting techniques for and lite covenants in leveraged loans and collateralized loan obligations.

An space I keep on to be anxious about are companies’ rosy assumptions about their Earnings Before Curiosity Tax and Depreciation (EBITDA). According to the Office environment of Money Study (OFR), earnings adjustments (also called EBITDA add-backs) generally took “the type of projected expense price savings extra back to earnings for the reason of expanding projected income and lowering the borrower’s leverage, or credit card debt-to-EBITDA ratio.” The Financial Steadiness Board has stated that these add-backs “were typically uncertain, in both equally magnitude and timing, and may well overstate a borrower’s EBITDA and as a result understate its leverage.” Typical and Poor’s in a assessment of companies’ EBITDA adjustments for 31 transactions in 2016 confirmed that, on ordinary, the companies’ projections ended up about 30% better than their true EBITDA.

When COVID-19 struck, credit history rating company downgrades of leveraged financial loan downgrades hit report highs moreover, defaults throughout most sectors of the economic climate greater noticeably. In contrast, the GAO uncovered that as of September 30, 2020, “senior CLO securities had generally retained their rankings, and the leveraged financial loan and CLO marketplaces appeared to be recovering.” Additionally, according to the GAO “based on the Federal Reserve and SEC staff’s assessments, write-up COVID-19 shock asset product sales from mutual cash that make investments mainly in leveraged loans could have contributed to downward stress on personal loan rates in an presently declining marketplace but experienced not posed a important danger to money steadiness as of September 30, 2020.”

Banking companies and other fiscal establishments are significantly interconnected.

Even though I am quite happy that leveraged loans and CLOs do not presently current a menace to monetary stability, I carry on to inspire financial institution regulators, the SEC, and FSOC to obtain a lot more facts about the interconnections between non-banks and banking companies in leveraged lending and CLO transactions. There proceeds to be a lot of opacity in these markets which helps make it complicated for buyers, regulators and taxpayers to get a entire perspective of how pitfalls in these markets could conclusion up impacting the money system and taxpayers. The U.S. GAO employees unquestionably ought to have praise for all the energy and time that they expended on this critical investigation.