hidden advantage for large companies signifies economic system has been K-formed for a long time

When the COVID-19 pandemic 1st strike, it appeared like the day of reckoning for in excess of-stretched company borrowers was lastly at hand. For decades, pundits and policymakers had been warning about a harmful develop-up of the credit card debt of “non-money firms”, meaning all those people that aren’t in finance, coverage or assets.

According to an OECD report frmo 2019, their credit card debt doubled globally in the decade following the crash of 2008-09. Undoubtedly the devastation wrought by a world-wide pandemic would be ample to pop this big bubble, placing off a wave of company defaults and putting the worldwide economic system at hazard of another main disaster?

However corporate default fees climbed throughout the entire world in 2020, the extensive-expected collapse of the company financial debt industry has not arrive to pass – at the very least not but. This is many thanks to govt intervention, especially the unprecedented moves by central banking companies, which include the Lender of England, to preserve the interest rates on corporate bonds reduced by specifically getting them.

These aggressive measures may have assisted to avert a company personal debt catastrophe, but they’ve appear at a hefty selling price. In 2020, global corporate personal debt issuance arrived at record highs, stoking fears that central financial institutions have merely delayed the inevitable.

Central banking companies to the rescue?

The steps also look to be fuelling a “K-formed recovery” from the pandemic, as substantial businesses revive and their smaller sized counterparts preserve falling. This is since central bank purchases have been greatly biased towards expenditure-quality personal debt, which is issued by big corporations with a lot more robust balance sheets.

SewCream

This has meant that corporate giants have been borrowing broad amounts at document small expenditures, whilst their more compact counterparts have struggled to elevate resources to see them by way of the pandemic. With these dynamics at enjoy, it appears to be virtually certain that in the submit-COVID earth there will be an improve in corporate concentration as much more modest gamers get absorbed by the giants.

Nevertheless indicators of a K-formed restoration are much less shocking than most people today possibly realise. The financial state has in point been K-formed for many years. As our new study on the US displays, the economic fortunes of massive firms have been steadily increasing considering that the early 1980s, while lots of smaller firms have fallen into acute fiscal distress. The pandemic, in other words, is intensifying longstanding dysfunctionalities in US capitalism. The pretty thought of a K-shaped recovery obscures this truth.

The K-shaped restoration in context

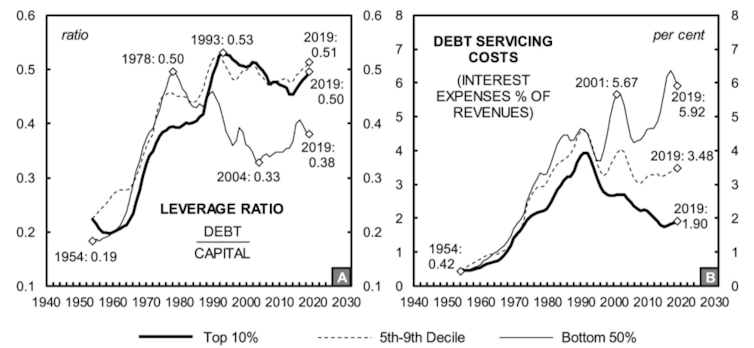

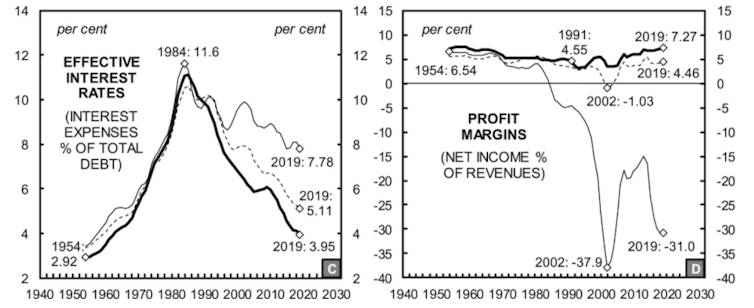

The problem can be viewed in the graphs beneath. Centered on US non-monetary businesses listed on the inventory current market from 1954 to 2019, they map their leverage ratios (credit card debt as a proportion of money), credit card debt-servicing prices, the fascination premiums they are efficiently having to pay, and web income margins. The traces in each and every graph depict the top rated 10% (in daring), the next 40% (in dashes) and the bottom 50% (in simple black) of organizations centered on their revenues.

We see that the borrowing ranges (leverage) of the major 10% have increased due to the fact the mid-1980s, whilst their financial debt servicing expenses and powerful fascination costs fell. In line with these fortuitous borrowing problems, the gain margins of huge companies doubled from just around 3.1% in the early-1990s to 7.3% in 2019.

Sandy Hager/Joseph Baines/New Political Economic system

What’s astonishing is that the base 50% lessened their borrowing above roughly the exact time period, but their personal debt servicing costs enhanced. In excess of this time, lesser businesses observed their profit margins dip persistently into destructive territory. The a long time-extended fall in fascination premiums seems to be the only matter that has stored more compact organizations afloat.

Smaller sized organizations hence appear to be caught in a vicious circle. The fact that their credit card debt-servicing burdens have enhanced sharply inspite of deleveraging and slipping interest fees details toward swiftly deteriorating fiscal fortunes. This is reaffirmed by the critical losses registered in their detrimental income margins.

More compact organizations may have been tempted to consider advantage of slipping fascination rates on borrowing to increase their revenues and profits. But the value of borrowing for smaller firms has been significantly better than for medium-sized and huge businesses, putting them at a considerable drawback.

For large firms, on the other hand, the circle is virtuous: higher and steady revenue margins allow for them to problem investment-quality bonds and borrow from banking institutions at lower curiosity premiums, which, in change, reinforce large and secure revenue margins.

Shareholder capitalism

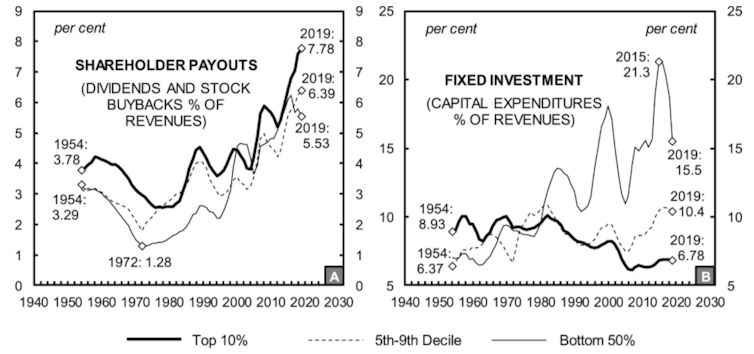

How did we conclude up in this circumstance? To deal with this question, we have to take into account the peculiar dynamics of shareholder capitalism as they have evolved in current many years. The graphs beneath chart shareholder payouts and mounted expenditure as a proportion of revenues for our sample of US non-fiscal businesses – once again with 3 distinct strains symbolizing the leading 10%, the upcoming 40% and the bottom 50% of organizations.

Sandy Hager/Joseph Baines/New Political Financial system

This displays that, in current many years, firms of all measurements have been under pressure from economic marketplaces to raise payouts to shareholders in the form of dividends and stock buybacks. But numerous of the greatest firms get pleasure from these types of a dominant position in the economy that they can return vast sums to shareholders without partaking in the massive-scale investments that may lead to lengthy-phrase work and wage development.

Corporations in the base 50% also have to appease shareholders who are frequently demanding higher returns on their investments, but in contrast to large firms they on top of that have to build on their own through huge-scale capital investment. This twin imperative puts them in a really precarious place.

So even though we may perhaps be witnessing a K-formed restoration from COVID-19, it is crucial to continue to keep in brain that this K-condition has a substantially for a longer period heritage. Though extra investigate is wanted, there are symptoms that this K-condition has also characterised numerous other innovative economies in the direct-up to the pandemic, together with the British isles.

In our check out, the pandemic signifies a missed opportunity for policymakers. Relatively than use their fiscal and financial electricity to develop a much more stable and equitable economical method, central banking companies rather have picked out to prop up a very dysfunctional just one.

Unless there is a radical departure from the recent coverage routine, the submit-COVID 19 globe is possible to resemble the pre-COVID 19 a single, only with much more industry turmoil simply because of the precarious placement of smaller sized businesses, far more focus, and even significantly less financial investment.