Taking A Gander At GreenSky (NASDAQ:GSKY)

")

Today, we take a rare foray into the fintech arena to look at a very beaten-down name in this space. I got some comments on this name recently from a follower asking for an in-depth analysis. A full deep dive follows in the paragraphs below.

Company Overview:

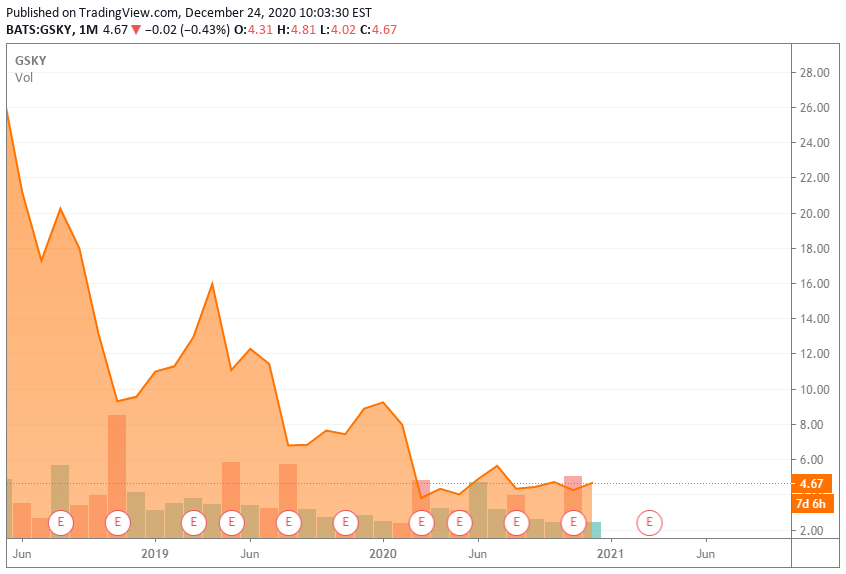

GreenSky Inc. (GSKY) is an Atlanta-based financial technology company that leverages its platform to connect an ecosystem of merchants, super-prime consumers (weighted-average FICO score: 784), and bank partners to process unsecured consumer loan transactions at nearly credit card processing speed. The company focuses primarily on the home improvement vertical and recently expanded into elective healthcare, boasting ~16,000 active merchants, ~3.6 million cumulative customers, and ~$26 billion of loan originations since inception. GreenSky was formed in 2006 and went public in 2018, raising net proceeds of $954.8 million at $23 per share. Beset with concerns regarding banking partners and decelerating growth before the advent of the pandemic, GreenSky has been a train wreck for investors on the IPO. The stock currently trades at just over $4.60 a share with an approximate market cap of approximately $830 million.

Source: Company Presentation

There are two classes of GreenSky stock: 76.4 million shares of publicly-traded Class A (as of Oct. 31, 2020), which confer one vote per share, and 106.2 million shares of Class B, which confer 10 votes per share, yet no economic interest. However, they are convertible into Class A shares on a one-for-one basis.

Business Model

GreenSky generates ~75% of its revenue acting as a broker, connecting consumers with lending banks through its network of merchants at the point of sale. For example, a homeowner needs to install a new door. On the recommendation of his/her contractor, the homeowner downloads the GreenSky app, which offers a financing deal. The contractor then scans the homeowner’s GreenSky ID on his/her mobile phone or tablet. The homeowner then provides other financial information and submits his/her application. The transaction data are sent to GreenSky, which tries to match the prospective borrower with its bank partners based on their underwriting criteria. Once a match is found, usually in a matter of seconds, the loan is approved. For providing this middleman service, GreenSky collects a transaction fee, which is paid by the merchant. That fee, which usually falls in the 6.5-7.5% range, is contingent upon the terms of the loan and was responsible for 77% of the company’s 2019 top line.

Source: Company Presentation

GreenSky also receives fees on loan portfolios it services on behalf of its bank partners plus incentive payments when the finance charges billed to borrowers exceeds the sum of an agreed-upon portfolio yield, a fixed servicing fee and realized credit losses.

This platform is touted as a win-win-win for each player in the ecosystem. The merchants benefit from increased sales volume and quicker payment. The consumers receive financing at rates superior to those provided by their credit cards while preserving the liquidity available under those cards. The bank partners get access to nationally diversified small-balanced loans at favorable net interest margins with no acquisition costs. GreenSky benefits as its merchant base uses its platform for a greater percentage of its transactions, providing it with low customer acquisition costs. Its nearly decade-and-a-half of loan data from super-prime borrowers engenders trust from its banking partners, helping build a moat around its unsecured loan brokering business.

As such, GreenSky is dependent on a small subset of merchants, sponsors, and banking partners for a large portion of its revenue. This leverage is especially true with the company’s banking partners, of which it only has eight. The top four (Bank of Montreal’s (BMO) Harris Bank, Fifth Third Bank (FITB), Truist Bank (TFC), and Synovus Bank (SNV)) were responsible for 80% of the commitments to originate loans as of Sept. 30, 2020. On the sponsor side, Renewal by Andersen represented 16% of GreenSky’s 2019 revenue, while Home Depot (HD) was its largest merchant, accounting for 4% of its business.

Issues:

The model would appear simple enough, but requires funding commitments from its banking partners, demand from consumers, and a strong base of point-of-sale locations. With a small number of banking partners providing loans, these relationships are essential, as without them, GreenSky can’t generate any fee income. It then also logically follows that an increase in the availability of these consumer loans is a precondition for growing its top line, short of a fee increase. In 2019, one of the company’s large banking partners, Regions Bank (RF), decided to step away from the indirect consumer lending business, ending its relationship with GreenSky in November 2019. After increasing its total funding commitments by $3.8 billion to $11.8 billion (of which $4.8 million was untapped) in 2018, the company realized a decline to $9.0 billion ($2.2 billion) at YE19. Keep in mind that these funding commitments are revolving and replenish as outstanding loans are paid down. Either way, the loss of Regions Bank in 2019 hurt perceptions of GreenSky’s business model and shed light on the short-term nature of the these funding commitments, which usually have automatically renewable one-year terms, are non-exclusive, and can be terminated for convenience.

The other requirement the company needs to increase its revenue is rising demand for the financing products it’s peddling. That element has been hurt by the economic shutdown, which has caused consumers to postpone or cancel nearly all elective healthcare procedures – which constituted ~10% of GreenSky’s originations pre-pandemic – offset partially by resilience in the company’s home improvement vertical.

The company also actively decreased the number of active merchants on its platform from 17,216 at YE19 to ~16,000 as of Sept. 30, 2020, by removing underperforming (i.e. less active) ones.

In theory, GreenSky could have increasing revenue in a flat supply and flat demand environment if it were able to increase its fees for brokering these transactions, but these fees have hovered around 7% over the history of the company, give or take 50 basis points. However, these fees can be negatively impacted by incentives. For example, it offers many loans with zero interest promotional periods of 12, 18, or 24 months, on which the consumer is billed interest but is not obligated to pay during the promotional period. If the customer then prepays the loan in full before the end of the promotional period, GreenSky is on the hook to remit the accumulated billed interest to its bank partners (less any budgeted incentives), even though none was collected. These promotional charges are captured in the Cost of Revenue line of the Income Statement as finance charge reversals (FCRs). The perception that these incentives, which many of its super-prime consumers can afford to prepay – thus, negatively impacting the company’s bottom line – were necessary to attract additional business also hurt GreenSky’s stock price.

Also adding to confusion regarding the company’s business model is its loan participation and whole loan sales, which have the effect of recycling its bank partners’ funding commitments. GreenSky, as part of its contracts with some of its bank partners, is obliged to sell these loan participations and whole loans. This is accomplished through a special purpose vehicle (SPV) facility, which receives the loan participations and whole loans the company helped originate and sells them at a discount to face value to the marketplace. The discount in the transaction increases the GreenSky’s Cost of Revenue line but recycles the capital, making it available for more loan transactions while reducing FCRs. GreenSky still earns the servicing fees on the loans it sells. These sales and obligations to sell work as long as the transaction fee (normally 7%) is greater than the discount in the transaction. To that end, Green Sky announced on Oct. 23, 2020, that it had sold $775 million of loan participations and whole loans through its special purpose vehicle for $0.95 on the dollar, most of it during 3Q20.

3Q20 Results and Outlook:

GreenSky then reported its 3Q20 earnings on Nov. 8, 2020, featuring Adj. net income of $0.03 a share on revenue of $142.0 million vs. $0.20 a share on revenue of $153.5 million in the prior year period. Most of the decline was related to its elective healthcare vertical being rubbed out during the pandemic. Adj. EBITDA increased 17% to $38.7 million as margins improved from 22% in the prior year period to 27%. However, that improvement was accomplished by adding back a newly-created $18.3 million line item reflecting a mark-to-market adjustment on future SPV commitments, the interest on which added $7 million to its top line. Owing to the collapse of its elective healthcare business (a.k.a. Patient Solutions), transaction volume was down 10% to $1.5 billion, but up 9% sequentially. Management indicated that 4Q20 origination volumes would be consistent as a percentage of total annual volumes versus 4Q19, or down ~7%.

Source: Company Presentation

On the positive side of the ledger, post-quarter close, GreenSky announced a new bank funding partner relationship, totaling $600 million a year over the next three years earmarked for Patient Solution loans, adding to $3.8 billion of funding renewals announced since the close of 2Q20.

Source: Company Presentation

Balance Sheet and Analyst Commentary:

On Sept. 30, 2020, the company’s balance sheet reflected unrestricted cash of $113.6 million and $453.3 million in debt. Loan receivables held for sale totaled $543.3 million against $432.8 million in its SPV facility obligation. The company utilizes its free cash flow to buy back stock, purchasing 8.7 million shares at a cost of $102.2 million during the first nine months of 2020. It does not pay a dividend.

Source: Company Presentation

Despite aggressively repurchasing its shares, GreenSky is universally loathed by Street analysts, who harbor five hold, three underperform, and two sell ratings and a median 12-month price target of $4 per share. During the 3Q20 conference call, they asked questions that displayed their uncertainty with (or perhaps ignorance of) the company’s business model.

By contrast, the company’s CEO, Chief Accounting Officer, and SVP of its Patient Solutions division all purchased GreenSky stock post-conference call, the most noteworthy of which was CEO David Zalik’s buy of 1.1 million shares at ~$3.47.

Verdict:

GreenSky’s share price reflects just under a 15 P/E on 2021E EPS of $0.28, entrenched near the bottom of a $3.05 to $9.84 52-week trading range. The EPS forecast reflects the Street’s uncertainty regarding the company’s business model and its ability to grow. Based on $1.5 billion in unused funding commitments as well as $2.1 billion in additional revolving capacity over the next 12 months coupled with management’s portrayal of bank partner interest on the conference call, there’s no shortage of capital to loan out. The question is whether the demand will return in the company’s Patient Solutions division. The bullish bet here is that elective procedures return markedly in 2021, rendering analysts’ estimates conservative and the stock undervalued.

I think there’s enough here to merit a very small “watch item” position which is what I did within my personal accounts. However, there’s too much uncertainty around this company in my opinion to merit for any larger stake than that. In addition, the Russell 2000 is having one of the best months in its history. I feel small caps are more than ripe for at least some significant profit taking in the weeks ahead, as is the overall market in my opinion. The better part of valor is discretion for the moment.

Bret Jensen is the Founder of and authors articles for the Biotech Forum, Busted IPO Forum, and Insiders Forum

Author’s note: I present and update my best small-cap Busted IPO stock ideas only to subscribers of my exclusive marketplace, The Busted IPO Forum. Our model portfolio has crushed the return of the Russell 2000 since its launch in the summer of 2017. To join the Busted IPO Forum community, just click on the logo below.

Disclosure: I am/we are long GSKY. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.