The Worrisome Financial debt Traits of More mature Us residents

For several older People, day to day life is turning out to be more and more precarious monetarily. A major explanation: As well substantially debt.

Credit score: Adobe

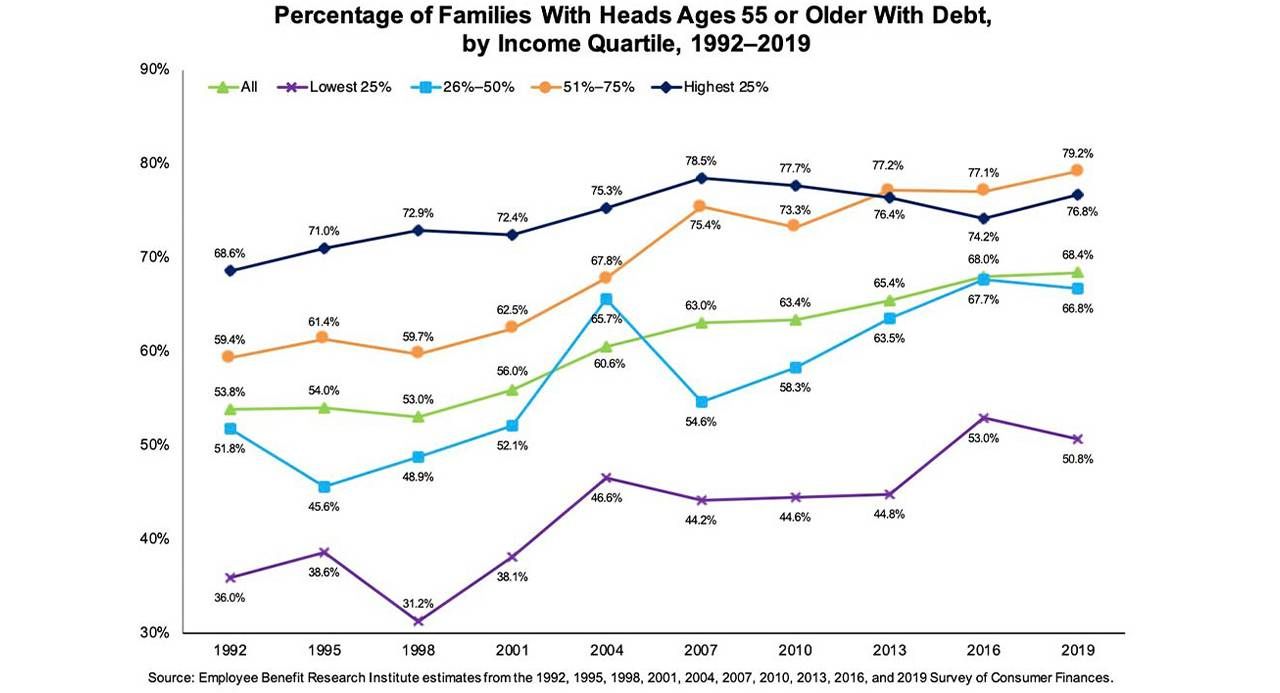

The numbers are placing. The share of family members headed by individuals 55 and more mature with financial debt is up from 54% in 1998 to 68% in 2019, according to the Personnel Gains Investigate Institute (EBRI). And retirees doubled their credit card debt in 2020, in accordance to the private finance internet site, Clever.com.

“To be carrying debt — important quantities of debt — at older ages will get riskier and riskier.”

“Personal debt is so substantially extra appropriate culturally,” states Jacquette Timmons, a monetary behaviorist primarily based in New York Metropolis.

The worrisome facet of debt among older older people mainly demonstrates the nation’s wealth and earnings economic bifurcation, even before getting into account how the pandemic has further more amplified inequalities in livelihood and opportunities.

Credit card debt Masses and ZIP Codes

Debt between the haves is very unique from debt among the these that have less. Persons dwelling in wealthier ZIP codes tend to minimize their money owed as they age, note Urban Institute economists Barbara Butrica and Stipica Mudrazija in “Financial Protection at More mature Ages,” printed by the Middle for Retirement Exploration at Boston College.

In sharp distinction, a lot less wealthy more mature grown ups with financial debt practical experience a significant improve in bank loan values relative to their belongings, say Butrica and Mudrazija.

Disturbingly, they obtain that bigger indebtedness (mortgages and credit playing cards) is now most pronounced between people 70 and older. Claims Butrica, an Urban Institute economist: “To be carrying personal debt — major quantities of debt — at more mature ages gets riskier and riskier.”

The credit card debt hundreds for quite a few older grown ups usually means “they’re residing on the edge,” says Pamela Foohey, going to professor of law at the Cardozo School of Legislation.

The threat that credit card debt could change harmful with age is greatest amongst specified teams of Us citizens, which includes minorities and those people with low-wage careers.

Says Odette Williamson, employees legal professional at the Boston-primarily based Countrywide Customer Regulation Centre. “More mature older people are using credit cards as aspect of their basic safety net to purchase medications. Or they just have to have foodstuff and other fundamental goods.”

Older grownups residing in a lot less-perfectly-off neighborhoods carry credit card debt very well into retirement, suggesting they may perhaps count a lot more on personal debt to guidance by themselves. And more mature minorities with credit card debt are additional susceptible fiscally than their white peers, according to the modern EBRI analyze, “Who Is Most Susceptible to the Ticking Financial debt Time Bomb in Retirement.”

Among the placing findings in that report: family members with Black or Hispanic heads 55 and more mature are a lot more probable to have customer debt (auto loans, particular financial loans and credit history cards) than housing credit card debt. The latter, nonetheless, features the possible for constructing prosperity.

Families with more mature minority heads of home, EBRI stated, had been extra possible to have personal debt payments accounting for extra than 40% of their income.

“For older grown ups of shade, the economical tension is relatively rigorous,” says Williamson.

Rising Bankruptcies of More mature Older people

An additional signal of debt worry amid more mature People: their increasing bankruptcies. One in eight individual bankruptcy filers is now 65 or over. That is almost a 5-fold maximize in just 2 ½ decades, according to the authors of “Graying of U.S. Bankruptcy: Fallout from Existence in a Threat Modern society.”

The major reasons more mature persons now file for individual bankruptcy are declining incomes and steep professional medical costs. Personal bankruptcy allows them discharge money owed though remaining in their house. States Foohey, a person of the paper’s co-authors, “They truly want to continue to keep the residence.”

A recent study by Fidelity Investments located that university student loan financial debt rose very last year among boomers, Gen Xers and millennials.

Some older Individuals are also having to pay off scholar financial loans — their individual or ones they took out for their kids’ tuitions. And student financial loans can’t be discharged in bankruptcy.

A new survey by Fidelity Investments found that university student financial loan credit card debt rose previous 12 months among the boomers, Gen Xers and millennials. Boomers lead the pack with an normal mortgage harmony of $58,000 and an typical monthly payment of $605. (University student personal loan payments have been suspended for the duration of the pandemic payments will resume at the conclusion of January except the moratorium is prolonged.)

How did we get to a spot exactly where older Us citizens are getting on far more credit card debt immediately after the prior generation aimed to enter retirement personal debt totally free?

Mainly, it stems from a disturbing social transformation above the previous generation dubbed the “terrific threat change” by Yale College political scientist Jacob Hacker. With businesses and govt sharing a lot less of the downside money dangers of previous age these times, substantially of the responsibility now lies with persons.

The basic illustration of the wonderful chance shift is Company The us abandoning pension ideas for 401(k)s. With pensions, the employer bears the expense danger and commits to a preset payout of cash in retirement. The 401(k) puts the chance on employees, like how considerably to commit and where by. Even worse, 40% of personal sector workers get the job done at providers that really don’t offer retirement discounts programs.

So, some people now borrow far more to test and keep their normal of residing.

Fiscal analysts say it’s time to get these debt complications very seriously simply because of the pandemic.

What Could Assistance Tackle the Credit card debt Challenge

Says Asha Srikantiah, head of Fidelity Investments pupil personal debt application: “What may have been manageable strain before, we have to view very carefully.”

Reversing the credit card debt craze will never be uncomplicated. But some kind of universal health and fitness care, common retirement price savings and universal long-term treatment aid would be a get started. The Biden administration is poised to get extra intense on all these fronts.

“The factor that needs to alter is to shift the risks again on to society,” claims Foohey. “It is really Variety 1.”

A quantity of states have begun offering retirement discounts options to employees of enterprises that don’t offer them. A couple are even stepping up to give extensive-expression care assistance.

Employers could also enable reduce personnel heading into debt by presenting workers payroll-deduction personal savings accounts different from their retirement ideas. The crisis savings cash could be tapped when wanted. A couple enterprises have introduced these kinds of systems.

Says Craig Copeland, senior investigate associate with EBRI: “I feel the pandemic brought the difficulty of unexpected emergency hard cash to the forefront.”

Democratic Senator Elizabeth Warren, a observed individual bankruptcy qualified, has an intriguing thought for bankruptcy reform. She’d get rid of the two most important forms of client personal bankruptcy — Chapter 7 and Chapter 13 — and substitute a new streamlined and productive one particular, Chapter 10.

Underneath Warren’s program, folks in individual bankruptcy with tiny debt could get an speedy discharge. All those with money obtainable to spend collectors would owe a bare minimum payment over a few a long time. And college student financial loans could be discharged in Chapter 10 bankruptcy.

You will find some fact to the observation that the American Desire was acquired on the installment plan. Yet there also demands to be one thing of a cultural transformation to enable reverse the terrific chance change.

Meantime, if you happen to be 55 or more mature, pay attention to what your grandparents said: Enter your later on yrs financial debt-absolutely free if you can.