Uncovering Apollo’s Real Financial Health During Stressful Times (NASDAQ:AINV)

")

Understanding Apollo Investment Corporation’s (AINV) real financial health during this uncertain economic time is of most importance. The company is a business development company (BDC) transitioning toward a high leveraged, lower risk investment model. It is targeting investments with 100% floating rates, primarily 1st lien, with a leverage ratio between 1.4 and 1.6. The company seeks to invest in businesses that are less susceptible to business cycles. Since 2015, the company has marched forward in this direction almost achieving its objectives. Its borrowing strategy allows most of its debt to float with the LIBOR index, up or down. It maintains an interest rate floor for its floating rate investments. In essence, the rate of return remains constant regardless of LIBOR values or market interest rates. We believe that this is a compelling approach for long-term investors seeking dividends. Apollo generates steady amounts of cash regardless of changes in the credit markets.

From the quarterly results, Apollo earned (NII) $0.43 in September, several cents above consensus, but down significantly ($0.59) from the peak in March. We wanted to know why.

A Short Description of BDCs

Over the past few decades, BDCs morphed into banks filling in what is referred to as middle sized loans, larger than small business but smaller than large bank loans with major corporations. BDCs began some decades ago by lending at high rates to companies under financial stress.

This business model generates high yields by borrowing at modest rates generally at 2-4% and lending at higher rates of 8-10% for 1st lien positions and plus 10% for 2nd liens. The government has set guidelines limiting debt to equity ratios labeled leverage. The rules define a ratio of 1 when assets are twice the debt. A ratio of two occurs with debt and assets roughly equal.

Recent History

Prior to the end of the March quarter, Apollo progressed methodically, reaching what we believed would be its maximum NII earnings at $0.59 in March with a leverage ratio equaling 1.71. Its leverage at the end of March was significantly higher than the high end of the company’s target. The company faced either deleveraging through economic patience or through generating capital from assets sales. Management chose the later. Since the end of March through November, assets were sold without requisite purchases. By November, management reported a leverage ratio near 1.45. Assets also fell from $2.97 billion to $2.59 billion.

Forced or Unforced Deleveraging

In attempting to uncover the primary reason(s) for its asset value decline, we first examined asset values starting with the total followed by key businesses shown in the table below.

| Investments (Billion) | Assets | 1st Misc. | 2nd Pharma | 3rd Business | 4th Aircraft | Non-Core* |

| Dec. 2019 | $2.97 | $0.683 | $0.475 | $0.416 | $0.386 | $0.356 |

| March 2020 | $2.79 | NA | $0.466 | $0.360 | $0.349 | $0.267 |

| June 2020 | $2.64 | NA | $0.446 | $0.343 | $0.341 | $0.241 |

| Sept. 2020 | $2.59 | NA | $0.448 | $0.355 | $0.339 | $0.214 |

* Heavy in energy

The table uncovers modest declines in its most important top businesses, but significant erosion in the small, energy heavy, non-core business. We also note that values for the company’s critical core businesses also turned slightly upward in its last report.

With only modest declines in value, we next examined earnings versus leverage.

* Reported in the September conference call.

Earnings did drop with leverage but in a disjointed manner.

With earnings dropping significantly on a modest drop in leverage ratio, between March and June, we looked deeper into the non-accrual investments (ones no longer paying).

| Non-Accruals | Dec. 2019 | March 2020 | June 2020 | Sept. 2020* |

| Value at Cost | $60 | $60 | $180 | $140 |

| At Fair Value | $20 | $50 | $45 | $30 |

* Management noted that during the September quarter, no investments were added to the non-accrual list.

As expected, non-accruals on a value at cost basis tripled between March and June. The above table also notes that non-accrual receded modestly in the September, certainly a good sign. Still, the $80 million change from March to June doesn’t fully answer the steep drop in earnings.

With only modest asset value changes within major investment sectors, we looked even deeper into the report asset sales and purchases. The next table summarizes these transactions.

| Deleverage (Millions) | Sales | Purchases | Net Difference |

| March 2020 | $212 | $153 | -$59 |

| June 2020 | $337 | $17 | -$320 |

| Sept. 2020 | $180 | $17 | -$163 |

| Total Deleverage | -$542 | ||

| Company Asset Change | -$500 |

With only the measurable decreases within the energy group, it’s clear that Apollo chose to deliver itself through asset sales. Notice that assets dropped $500 million and the sell versus purchase difference amounts to slightly more at $540 million. The company noted at the last conference that the leverage ratio was low enough for the company to once again restart its purchasing.

Understanding Two Deeply Hurt Assets

It seems that Apollo found a bottom last quarter within its objectives. With its airplane leasing business at approximately 15% plus its heavily energy weighted non-core investment, the two together represent at least 20% of the total. Understanding the status of major issues for these two sectors is also important.

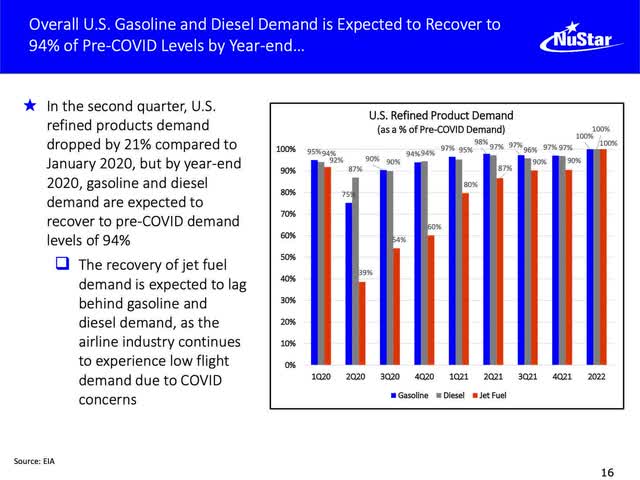

A slide from NuStar Energy’s (NS) last conference includes its estimate for the full return of crude product demand.

The grey line in the graph represents jet fuel demand, in essence, full demand for airplanes. At this point, demand is at about 60% of 2019 levels and expected to reach its 100% during the 1st quarter of 2022. This is an estimate, but helps us place a time frame for the recovery of Apollo’s airplane leasing company (Merx).

Merx Aviation’s yield fell from 12% to 10% during this period of stress. At $350 million, the change represents $2-$3 million per quarter in earnings or 10% of the total change. Over the next year or two, this should return.

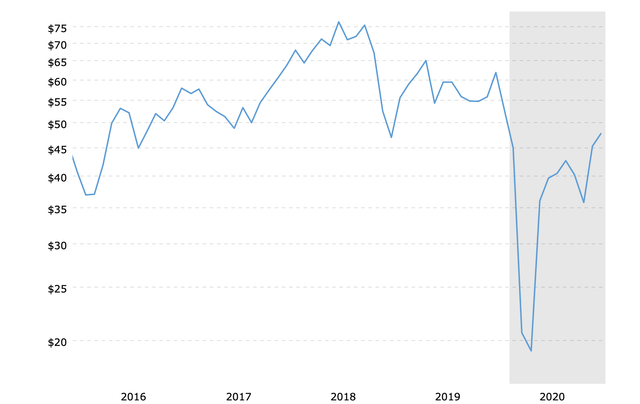

Crude oil pricing has already returned most of the way toward its December 2019 pricing shown in the chart below.

What hasn’t yet returned is demand, which is still 8% lower than last year. But the crude oil and product markets have improved significantly in the 4th quarter. With crude pricing returning, valuation of the energy heavy non-core assets should return. Two critical pieces of Apollo’s investment environment are healing.

Going Forward

The value of Apollo’s core businesses seems stable with its energy and airplane leasing business improving. Although it might take another year for the travel business to fully recover, the company is still producing earnings with what appears to be floor in place. When evaluating earnings for the past 4 quarters falling from $0.59 to $0.43 and the leverage bottoming at the high 1.40’s, we expect December’s earnings will reflect the floor. Our estimate for this quarter’s earnings might range between $0.37 and $0.43. We expect the company to continue paying approximately $0.35 in dividend, portioned between a special plus fixed.

What we didn’t find was the full reason for the significant drop in earnings. Our guess is that although only a few companies fell into non-accrual status, many others may have made limited payments. In time, we believe that this circumstance will heal.

Apollo’s modest drop in non-core asset values triggered the company to lower its leverage through significant asset sales. We expect Apollo to begin the repurchasing process for core assets, returning its leverage ratio into the high middle 1.50s beginning in the December quarter. Earnings at that level would likely continue to average between $0.45 and $0.50. We suspect that in time any partial payments will return. The time frame for recovery is likely 1-1.5 years.

We continue to hold a fairly large position with a significant piece under a dividend reinvestment program. We are particularly impressed with the financial model of this BDC, the debt/equity return naturally hedged for consistency regardless of interest rates. We find this compelling for a long-term strategy.

Disclosure: I am/we are long AINV. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.