Will Snap Ultimately Get to Profitability in 2021?

Snap Inc. (NYSE: SNAP) owns Snapchat, 1 of the most well known cell cellphone apps in the world. Folks enjoy applying the app remain in contact with good friends, share images, and take in information from social media creators.

Inspite of the reputation of the support, which introduced approximately a ten years ago, Snap has mainly been unprofitable. Having said that, the firm has seemingly turned a corner as it started reporting good EBITDA in the past yr. Can the company solidify its revenue streak in 2021, and could this travel the stock bigger?

Picture resource: Getty Photographs.

Snap’s soaring margins

By definition, a profitable company provides in much more cash than it lays out. And 1 way for a enterprise to come to be additional profitable is to choose in much more dollars in the sort of escalating revenue. Making use of this standard framework, it’s easy to see why Snap is generating development on its bottom line — the company is growing income at a fast fee.

In its 3rd-quarter earnings report, the corporation savored 52% year-about-yr revenue progress. This development fee would be outstanding in any atmosphere, but it is specifically exceptional specified that 2020 observed a global economic economic downturn.

Marketing fees declined last yr, but Snap has been in a position to much more than offset this headwind with potent user growth and much more adverts proven to just about every person on ordinary. Individuals are flocking to the app simply because of ample absolutely free time during the pandemic and Snap’s sturdy product innovation.

| Metric | Q3 2020 | Q3 2019 | YOY Improve (%) |

|---|---|---|---|

| Profits | $678.7 million | $446.2 million | 52% |

| Altered EBITDA | $56.4 million | ($42.4 million) | N/A |

| Web loss | ($199.9 million) | ($227.4 million) | N/A |

| Every day lively users | 249 million | 210 million | 18% |

| Average profits for every consumer | $2.73 | $2.12 | 28% |

Info resource: Snap money studies. YOY = year around year.

The profits growth at Snap is interesting, but probably even a lot more impressive is the company’s mounting profitability. As you can see in the third quarter, EBITDA came in at $56 million, reversing a $42 million decline in the prior-year interval. What is far more, that was the second time Snap claimed constructive EBITDA in the past four quarters.

What drove the turnaround? Larger scale authorized the company to increase its income faster than its bills. This is referred to as functioning leverage, and it really should keep on to gain the organization as it grows its best line.

Positive EBITDA but not yet “successful”

Snap has reported constructive EBITDA, but it even now has negative net income. In the eyes of a lot of traders, that suggests the enterprise is even now unprofitable. Having said that, the organization is a lot less unprofitable than it was a 12 months in the past and could report positive earnings in the coming quarters if it carries on to mature at a quick amount.

Even though EBITDA would not reflect all charges, traders like to use the metric, simply because depreciation and amortization are non-money bills (accounting adjustments), and businesses can have vastly distinct tax premiums and desire charges on credit card debt. Working with EBITDA will make it a lot easier to examine unique providers.

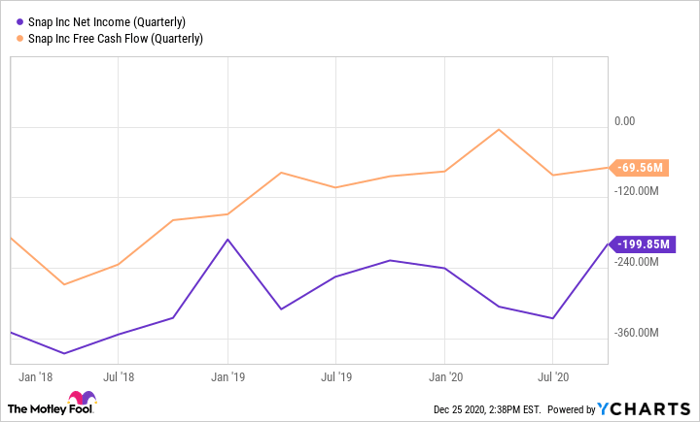

Knowledge by YCharts.

Net income is also an critical metric, since taxes and fascination on financial debt are genuine fees. Depreciation and amortization may possibly be non-cash, but they relate to cash expenditures, which are also authentic money bills.

Buyers can also change to free funds circulation as a proxy for a company’s earnings electrical power, since it measures real hard cash era devoid of the non-cash adjustments. As the chart previously mentioned shows, Snap has made development in improving both equally its cost-free cash circulation and net income vs . previous decades. Also interesting is that Snap’s cost-free cash movement is higher than its web profits. Yet again, this is simply because the firm’s non-funds fees (notably its inventory-primarily based compensation) are significant detractors from internet income.

Profitability in 2021?

As of now, Snap is firmly in the pink, but it has manufactured major progress in increasing its bottom-line metrics. If Snap can grow profits as significantly in 2021 as it did past calendar year, then it absolutely has a shot at reaching “genuine” profitability in terms of web revenue and cost-free money circulation. However, in an atmosphere with significant economic uncertainty, traders most likely shouldn’t rely on it happening way too before long.

On the lookout forward, the new year poses numerous prospects and problems for Snap. Even though the COVID-19 pandemic hurt numerous companies, Snap appears to have benefited to a degree from folks being at property. The enterprise could truly see slowing person advancement on the platform this yr as the financial system reopens. On the other hand, with the overall economy recovering, advertisers may possibly also have more self confidence to increase advertisement shelling out with Snapchat and other social media platforms. This latter scenario will be what traders ought to enjoy closely as they comply with Snap’s march toward profitability.

10 stocks we like much better than Snap Inc.

When investing geniuses David and Tom Gardner have a stock idea, it can pay to hear. Soon after all, the publication they have operate for more than a 10 years, Motley Fool Stock Advisor, has tripled the marketplace.*

David and Tom just discovered what they think are the ten ideal stocks for investors to get ideal now… and Snap Inc. wasn’t one of them! That is correct — they feel these 10 stocks are even much better purchases.

*Inventory Advisor returns as of November 20, 2020

Luis Sanchez CFA has no place in any of the shares talked about. The Motley Fool has no place in any of the stocks mentioned. The Motley Fool has a disclosure plan.

The sights and opinions expressed herein are the sights and opinions of the author and do not necessarily reflect all those of Nasdaq, Inc.