Will These Three Stocks Lead The Market In 2021?

/https://specials-images.forbesimg.com/imageserve/5fe8d4541bc4dcd83fdd8100/0x0.jpg "Will These Three Stocks Lead The Market In 2021?")

Bull market growth financial and positive investing success concept as a tree shaped as a symbol for … [+]

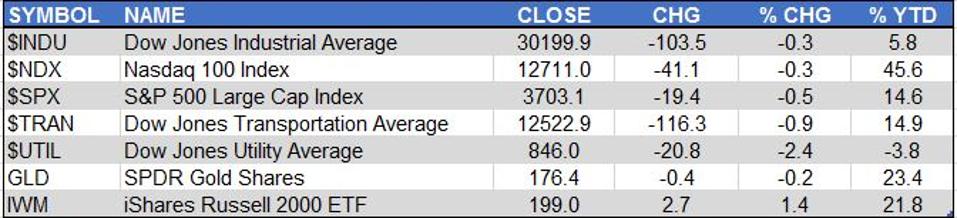

There was little pre-Christmas selling during Thursday’s abbreviated session. In light of the economic news from earlier in the week, this was especially a good sign. Monday’s Chicago Fed National Activity Index recorded the weakest reading since May.

This was followed Tuesday with a decline in the Consumer Confidence to 88.6, from 96.7 last month. This was consistent with the 0.4% decline in Consumer Spending.

On a percentage basis, the losses last week were

Markets

slight, with the Nasdaq 100

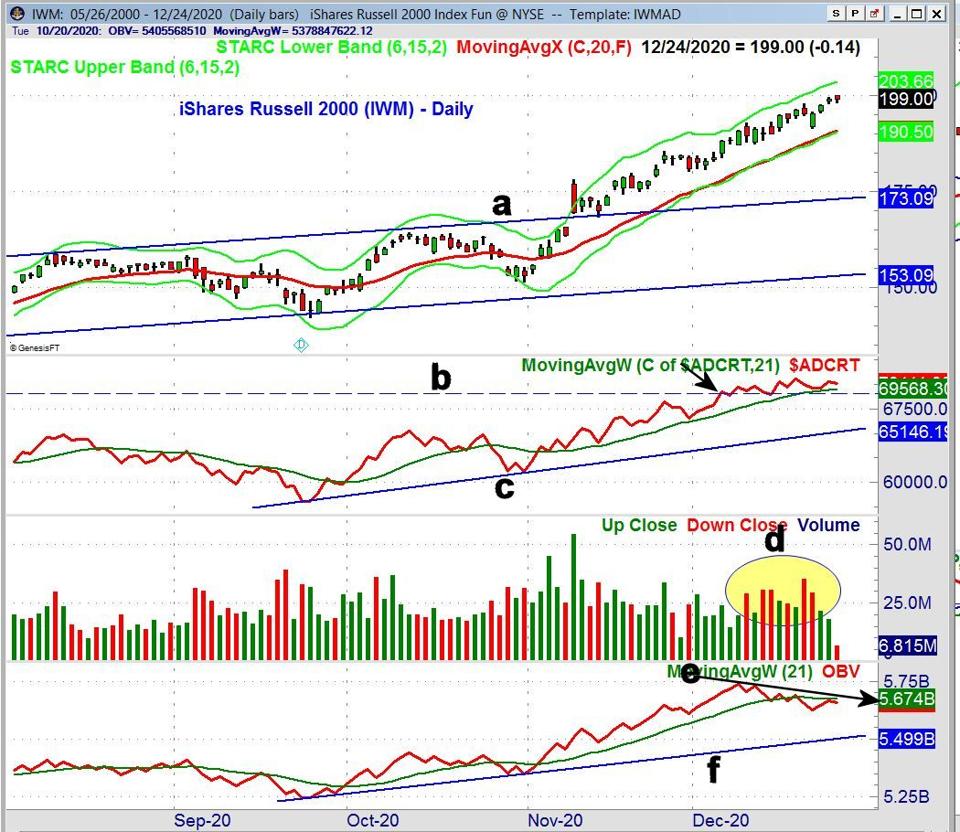

IWM

Over the past several weeks, IWM has not looked as strong as it did in November when it broke above resistance (line a) from its trading range. The fact that it has exceeded its weekly starc+ band for many of the past six weeks is a warning of increased risk. It closed last week at $197.77, over 4% above its 20-day exponential moving average (EMA). This means that even a 4% decline would not necessarily change the positive trend.

The Russell 2000 Advance/Decline line moved to a new all-time high on December 4, as the prior high (line b) was overcome. It did not make a new high last week and shows a short-term negative divergence from prices.

Over the past two weeks, there has been greater volume when IWM has declined than when it has moved higher, which is evident by the number of taller red bars (circle d). Therefore it is not surprising that the daily On Balance Volume (OBV) has started to diverge from prices (line e) as well, having peaked on November 8. The OBV is also now below its weighted moving average (WMA), but does show a positive trend from the September lows (line f).

The S&P 500 is a major benchmark for the stock market, which most investors and analysts follow. The Spyder Trust (SPY)

SPY

The weekly chart shows that the SPY completed its flag formation (line a and b) the week ending November 13. It formed a doji two weeks ago, which means that a week-ending close below the doji low of $364.47 would trigger a weekly doji sell signal. The rising 20-week EMA is currently at $348.14, acting as support 5.7% below last Thursday’s close.

The weekly S&P 500 A/D line made its high on December 4 and has formed slightly lower highs (line c) over the past two weeks. There is good A/D line support at the October high (line d) and the rising weighted moving average.

As of December 24, SPY is up 14.6% YTD. If it holds these gains that would make 2020 its fourth-best year of the bull market going back to 2009. For some perspective, 2013 and 2019 each had yearly returns of over 30%.

This year, one of the concerns is that “more than half the S&P 500’s gain this year has come from just three stocks: Apple, Amazon and Microsoft”. A look at the weekly charts of these three stocks may help us determine whether they will also be the major contributors to the S&P 500 in 2021.

Apple Inc

Apple, Inc

AAPL’s weekly relative performance (RS) versus the S&P 500 moved back above its WMA three weeks ago and is approaching the September high. Its On Balance Volume has been much stronger, making a new high each of the past two weeks.

AMZN

Amazon

Both of the weekly indicators, the RS and OBV, have been negative since October 23 (line c). That is when the RS dropped below its WMA, and on the rebound in early November, failed to turn positive. The OBV shows a similar negative pattern. Both indicators have been in downtrends since October (see arrows).

Microsoft

Microsoft

The weekly RS peaked in July and then violated support (line c) in the middle of November. The RS is now rising and could move above its WMA if MSFT is stronger than the S&P 500 this coming week. The weekly OBV has also improved recently and has rallied back to its downtrend (line d) and its WMA.

The weekly charts of all three stocks reveal that they are in continuation patterns. This gives all three stocks a positive bias, but that does not mean they can’t break to the downside before a further rally in 2021. AAPL looks the strongest from the weekly technical studies, while at this point, AMZN looks the weakest.

Apple reports its earnings on January 26, while MSFT reports the following week on February 3. With no strong evidence yet of a major top, these three stocks could again be the major contributors to the S&P 500 again in 2021.

In the Viper ETF Report and Viper Hot Stocks Report, I teach subscribers how to pick stocks or ETFs, and provide specific buy and sell advice along with market commentary. Each report comes out twice a week and is only $34.95 per month.