The Other Subsidy Relished By Massive Tech

/https://specials-images.forbesimg.com/imageserve/5ffe314d8a68ca21dafd18fd/0x0.jpg "The Other Subsidy Relished By Massive Tech")

SOPA Images/LightRocket by means of Getty Visuals

Earnings do not reflect how substantially employee stock payment expenditures shareholders

The COVID-19 pandemic and tried government insurrections apart, headlines these days are dominated by how Huge Tech’s expansion has been subsidized by the area 230 exception of the Communications Decency Act. And although portion 230 shields internet websites from lawsuits in case a person posts a little something illegal, I want to emphasis on a further concession liked by Massive Tech. It’s an arcane, but successful money reporting rule that permits companies to underneath-report the genuine charge of compensating their personnel.

So how is this possible? Tech providers rely on generous fairness grants to draw in and retain employees. Reporting guidelines enable these businesses to cost the projected reasonable values of these shares and possibilities on the day at which they’re granted. The real money circulation linked with these grants can be bigger relative to the compensation cost that exhibits up in companies’ revenue statements. However, the dollars outflow is obscured as payouts to shareholders are under no circumstances explicitly linked back to compensation expense. Tech corporations also really feel the strain to flip a financial gain to guarantee investors that they will improve into their lofty valuations.

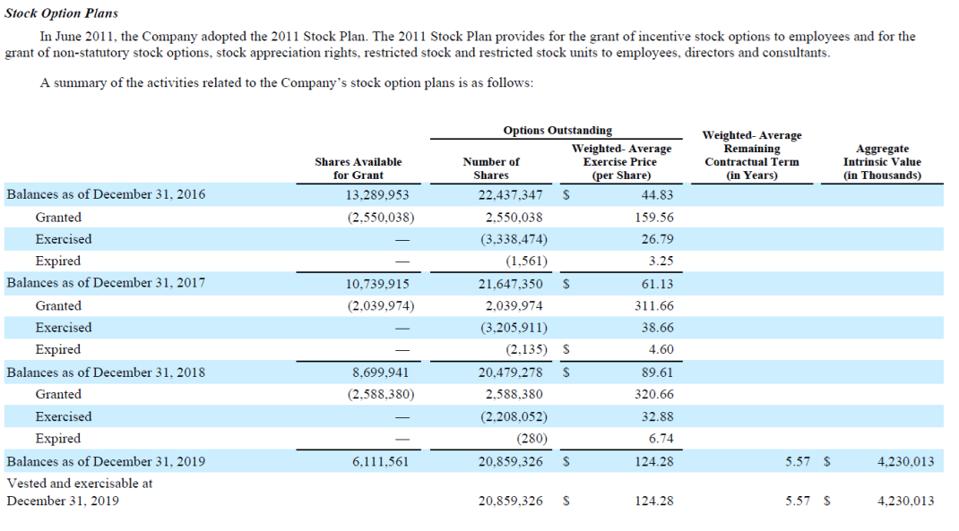

For instance, contemplate the circumstance of Netflix. I extracted the adhering to footnote associated to stock options from their 10K filed for the 12 months ending on December 31, 2019.

Netflix footnote

Think about the 2.208 million solutions exercised by staff in 2019. These alternatives were being issued at an training rate of $32.88. When personnel training these choices, Netflix requires to challenge share certificates to these staff members. Where do these shares occur from? Many hard cash abundant providers such as Google would get stock from the open industry to fulfill that need. Netflix needs all the hard cash it can get to devote in material output. So, it difficulties fairness to fulfill the demand for share certificates to its staff members. The normal share price at which Netflix traded in 2019 was $320.66 (assuming it is the exact same as the exercise rate at which selections have been granted in 2019). Hence, the shareholder price specified up by Netflix in 2019 to pay back its workers was $320.66*2.208 million shares or $708 million.

How substantially of this worth transfer to workforce is identified in Netflix’s cash flow statement as payment cost? That is rather tough to nail down. However, we do know that the “fair value” of these solutions on the grant day of the alternative is demanded to be expensed as for every U.S. GAAP (commonly approved accounting concepts). In basic, the “fair value” of the solution, supplied Netflix’s profile, is roughly half or a 3rd of the physical exercise price of the option. To help the argument from me, let’s go with 50 %. That would suggest that prior earnings statements of Netflix had been billed with compensation price of about $36 million (2.208 million shares*$32.88/2). Forgetting taxes for a minute, compensation price is under-reported by $672 million ($708-$36) relative to the value sacrificed by Netflix’s shareholders to its staff.

Before you consider this is insignificant, let’s benchmark the unreported expenditure to former year’s revenue numbers as these alternatives were being probably issued courting back again to 2017, 2016, or even before. The pre-tax cash flow for Netflix in 2017 was $485 million. The unreported payment expenditure therefore functions out to 139% of its 2017 described profits ($672/485 million). Hence, Netflix would have reported a decline in 2017 had the genuine charge of staff compensation been reported to shareholders.

There are countervailing arguments for positive. One could argue that the possibilities had been supplied back again in 2016 or 2017 when the upcoming operate-up in inventory selling price was not envisioned. Fair sufficient. But we routinely mark other fiscal devices to current market. Why should companies acquire write downs for marketable securities that have shed price?

The second objection I usually listen to is that giving workers possibilities back in 2016 or 2017 actually enabled Netflix to do properly and led to the massive run-up of its inventory price tag. That is undoubtedly doable. Assuming stock price ranges are at least loosely correlated with recognized general performance, Netflix’s results will display up as better revenues in its cash flow statement. Instead, why not replicate the greater expenditures of payment probably dependable for this sort of results? Moreover, would the stock have run up as substantially as it did if traders recognized the real price transferred to its employees? I am not absolutely sure, but it would be good to have these issues answered in exercise.